(Earlier posting on the 8th August – republished)

Australian (un)employment data released yesterday (7th August 2014) surprised many with a sudden spike in the jobless, especially in the State of Victoria. With Australia entering a transition period following the mining boom a “big” question is what Australia’s future economic strategy foundation should be in the new world order, especially with seismic disruptions from digital and technological innovations.

The latest newsletter of the Committee for Melbourne (Committee Communique, August 7 2014) contains an interesting statistic. Survey data undertaken by the World Economic Forum and the Boston Consulting Group (BCG) ranked, in comparison to other G20 states, Australia in the top 5 for early technology adoption (sounds good) but at or below 15th for business use of technology in innovation (sounds bad). This may reflect a willingness to be a consumer of technology but a corresponding failure to capitalize on “digital value creation”. A net outflow of value rather than an inflow.

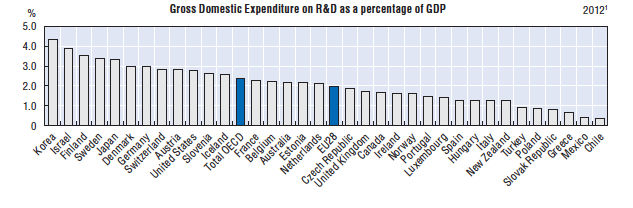

Further evidence for concern is our competitive position in R&D tables published by the OECD (Source: OECD Main Science and Technology Indicators Database, July 2014). While our general expenditure in R&D is slightly above the median:

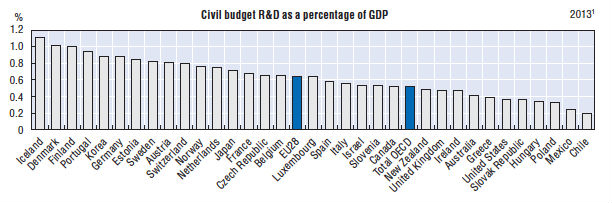

our R&D budget from non-government or university sectors is significantly below the median:

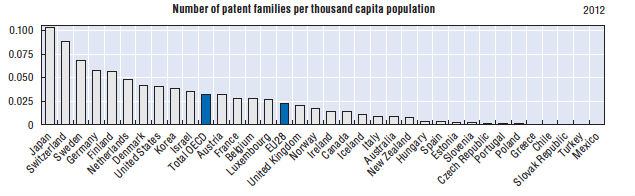

As for international performance in commercialising R&D Australia slips even further as shown in the number of patents (based on the triadic patent definition across three patent office regions – EU, US and Japan):

Arguably Australia is not reaping a fair commercial return on the overall R&D investment with some notable exceptions (e.g. Cochlear and CSL). In this case Australia is not hitting above its weight and may become more exposed to negative risk with evolving models, such as digital economies.